Social Security - Is it even worth it to plan for?

- William Hubbard

- Aug 1, 2025

- 5 min read

For nearly nine decades, Social Security has served as a cornerstone of American retirement security. However, as demographic shifts reshape our society, questions about the program's long-term viability have become increasingly prominent. While Social Security remains a vital component of retirement income, it represents just one element of comprehensive financial planning. Given today's economic and political landscape, understanding how all retirement planning pieces fit together is essential for achieving your long-term financial objectives.

Regardless of whether retirement is imminent or still years away, gaining insight into Social Security's role within your broader financial strategy is crucial. To make informed decisions about the opportunities and challenges ahead, it's valuable to examine the program's origins, current pressures, and available approaches for managing future uncertainties.

Social Security's evolution from inception to today

Created in 1935 amid the economic turmoil of the Great Depression under President Franklin D. Roosevelt's administration, Social Security emerged as a crucial safety net for America's elderly population. From its humble beginnings providing modest payments to a limited number of recipients, the program has transformed into an extensive system supporting millions of retirees, individuals with disabilities, and their dependents. Currently, Social Security benefits constitute a substantial portion of retirement income for countless Americans.

What obstacles does Social Security face in today's environment? The program functions mainly through a pay-as-you-go framework, where current workers' payroll contributions fund today's benefit payments. Put simply, the payroll contributions you make don't accumulate for your future benefits but instead support today's Social Security recipients.

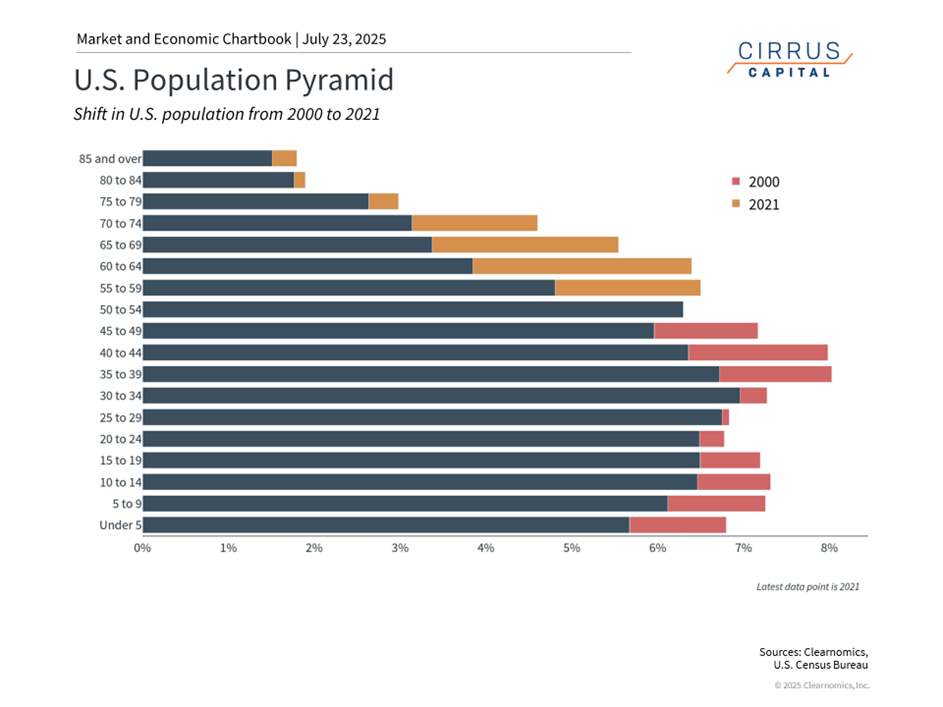

This approach functioned effectively when worker-to-beneficiary ratios remained favorable throughout most of the 20th century. Nevertheless, changing demographics have resulted in fewer workers supporting the system while more retirees claim benefits. To illustrate, 1940 saw 42 workers supporting each retiree, but today that figure has dropped to approximately 2.8 workers per beneficiary, with further declines anticipated as aging accelerates and birth rates remain low.

Numerous forecasts have attempted to predict when Social Security trust funds will face depletion. The most recent assessment from the Social Security Board of Trustees suggests reserves will last until 2034, beyond which benefit reductions would become necessary. Currently, continuing payroll contributions would still support roughly 78% of scheduled benefits. While specific timelines may vary, the fundamental challenge persists: absent reforms, the trust funds may struggle to deliver full promised benefits over the long term.

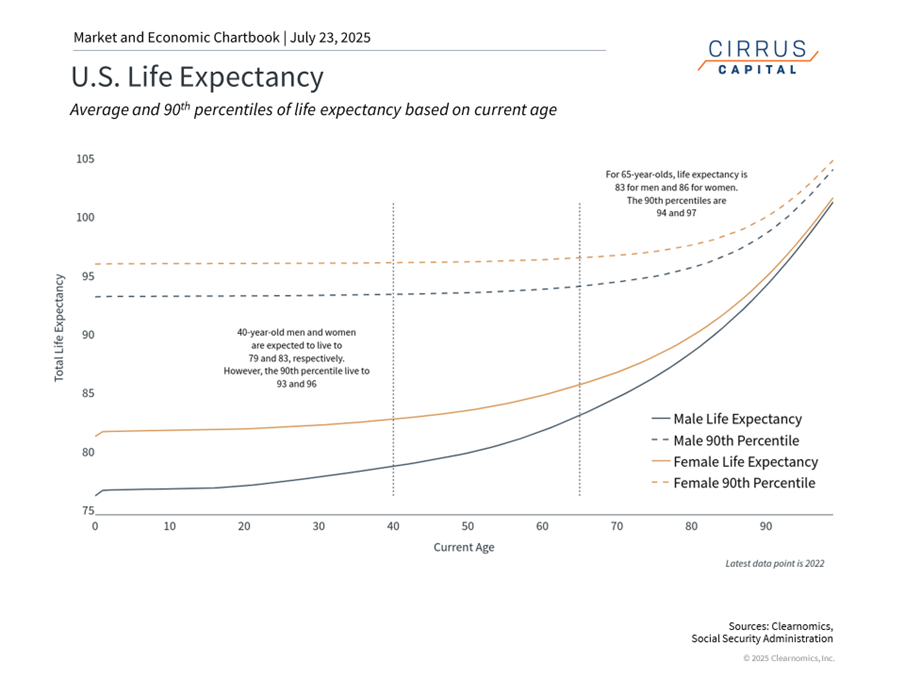

Increased longevity presents both opportunities and funding challenges

The national debt and deficit situation compounds concerns about program sustainability, with debt approaching $37 trillion while persistent deficits continue. Despite Social Security's "mandatory" classification, pressure to reduce government expenditures creates uncertainty about potential Congressional modifications to these programs.

Given the intense political debates surrounding potential solutions, a swift resolution to Social Security's challenges appears unlikely. Proposed remedies include adjusting retirement age requirements, expanding the taxable wage ceiling, and enhancing fraud prevention measures. Unfortunately, comprehensive long-term solutions for Social Security remain elusive.

Examining how other developed nations have addressed similar demographic pressures can provide valuable insights. Several European countries, including France and the UK, have raised retirement ages to alleviate system strain. Australia has implemented a different strategy through "means-tested" calculations that limit benefits to retirees meeting specific asset and income criteria.

Although the 2034 depletion timeline remains distant, the urgency for solutions will intensify. While complete benefit elimination seems highly improbable, ongoing funding pressures will likely necessitate program modifications.

Key Planning Considerations for Retirement

Focusing on individual actions, thoughtful planning becomes essential for maintaining retirement progress amid Social Security uncertainties. Optimal decisions depend on your comprehensive financial situation, objectives, tax circumstances, and additional factors.

Consider these important elements:

· The Delay Decision

While retirement benefits become available at age 62, claiming early results in reduced monthly payments. Alternatively, postponing benefits until age 70 can boost monthly payments by roughly 8% annually beyond full retirement age (66-67, based on birth year), per the Social Security Administration.

Conducting a breakeven analysis helps evaluate whether delaying represents a beneficial approach. Typically, living beyond your early 80s makes delayed benefits advantageous for lifetime payments. However, this calculation shifts when considering time value of money or opportunity costs.

· Bridge Approaches

The benefit of delaying largely depends on your income source during the waiting period. Some retirees utilize portfolio distributions as a "bridge" to enhanced Social Security payments later. This approach proves especially valuable for married couples, where optimizing the higher earner's benefit establishes a larger survivor benefit.

· Tax Considerations

Social Security benefits may be taxable up to 85%, based on your combined income level. Future tax legislation could potentially raise this percentage. Strategic withdrawal planning with professional guidance can help reduce the tax burden on your benefits.

· Prudent Assumptions

Individuals earlier in their careers have additional time for retirement preparation and more flexibility to adapt to Social Security uncertainty.

Therefore, younger workers might consider developing retirement plans that don't depend heavily on Social Security. This approach doesn't mean completely disregarding it, but rather viewing potential benefits as complementary to personal savings instead of foundational.

· Monitor Policy Developments

Policy modifications will probably occur before trust fund depletion. Staying current on proposed reforms enables appropriate planning adjustments. Potential changes encompass additional full retirement age increases, benefit formula modifications, or payroll tax cap alterations.

· Optimize Tax-Advantaged Savings

Given Social Security's uncertain future, maximizing 401(k), IRA, and HSA contributions becomes increasingly critical. These vehicles offer tax benefits that can help offset potentially diminished government benefits.

Navigating Social Security's Future Through Strategic Planning

Despite valid concerns, maintaining proper perspective remains important. Social Security has encountered funding difficulties previously, and political motivation to preserve the program continues strongly.

The sensible approach involves neither complete reliance on nor total dismissal of Social Security's retirement planning role. Instead, investors should acknowledge the program's significance while considering it as merely one element of a well-rounded retirement approach.

Interested in more of these insights? Drop us a line!

Disclaimer

Opinions are as of the published date and are subject to change without notice. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation to buy, hold, or sell any security. There are limitations associated with the use of any method of securities analysis. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance, and time horizon before making any investment. Prior to making an investment decision, we should have a conversation to see if a particular strategy makes sense for your situation. Investing involves risk, and you may incur a profit or loss regardless of chosen strategy or investment. Past performance does not guarantee future results. There is no guarantee that any statements, opinions, or forecasts provided herein will prove to be correct. Indices discussed or included are for informational purposes only. Investors cannot invest directly in any index. Contact me for further information.

Comments